Are you a Quiet Speculation member?

If not, now is a perfect time to join up! Our powerful tools, breaking-news analysis, and exclusive Discord channel will make sure you stay up to date and ahead of the curve.

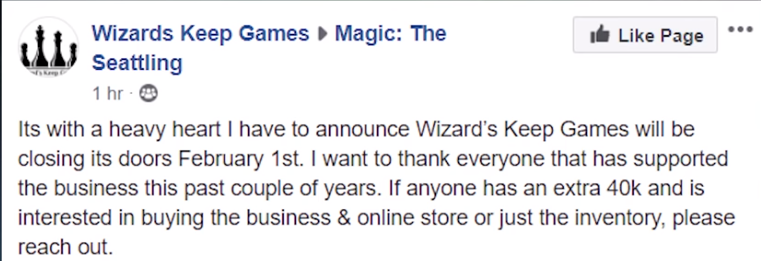

It's always sad to see a game store close. I have numerous great memories from my childhood while at my local game store (LGS). These are where I met my best friends and best men at my wedding. These are the places we go to when we want to relax and enjoy the company of people with similar hobbies and interests; where people of various backgrounds with a great many differences can bond over shared interests and realize that despite these differences we still have a lot in common. Their importance in the MTG Finance realm is paramount.

All that being said, I think one should take a step back and consider this statement. I don't know the background or history of Wizard's Keep Games, but I find it a bit hard to believe that the Secret Lair series was the straw that broke the camels back. I say this being one of the people who criticized WoTC for that series myself. I think WoTC has misevaluated the importance of LGS's to their own business model, but that is on them to figure out.

Every store needs to understand that WoTC has a monopoly on Magic: The Gathering and all their other franchises. They are going to do what they think will generate them the most income as all good businesses do. This means that WoTC's #1 priority is their own business growth. We've seen a lot of game stores pop up in large part due to Magic's massive growth over these 26 years, with many generating a significant amount of revenue with just Magic singles sales. In fact, that may very well be where our problem lies.

Magic singles are a very lucrative business. When you compare buylist prices to store retail price you often see profits of 30-50%, which is insanely high compared to almost every other industry. Now, to be fair, there are overhead costs that eat into those profits, but if you can turn over a large number of cards regularly those costs are minor profit reducers. So why is that the problem?

With singles being so lucrative, it makes sense that more and more people would want in on the market. The biggest bottleneck was how to convey your wares to the world. While we have almost always had eBay as an option, TCGPlayer opening up to non-B&M (brick and mortar) stores was the real game-changer. Now anyone can own a store with your competitor's prices readily visible, making pricing a lot easier.

To make matters worse for LGS's, these non-B&M stores have much lower overhead costs. This means they can price out many B&M stores that don't have enough singles sales to make overhead costs negligible. In this very real and unfortunate way, every one of us who sells cards on TCGPlayer but doesn't own a physical store presence is contributing to the downfall of the LGS.

The Great Debate

Interestingly enough, I often see two types of players debate this problem on social media.

One side argues that the higher cost of the cards is that the store provides additional value; the LGS provides an environment to play those cards, and if there were no stores, there is little reason to buy the cards. This is a legitimate argument, but one that likely obfuscates a potential root cause of a store's financial problems. This argument is only accurate to the point where the price difference equals the actual overhead costs + TCGPlayer low with shipping. Obviously, the buyer doesn't know the store's overhead costs, but it's important to understand that any copy of the same card has the same "play value," in that a copy of Sol Ring I buy from the cheapest store on TCGPlayer is just as playable as the copy I buy from my LGS.

This is important to understand, because we live in a society where people want the best deal. The definition of "best" will likely vary from person to person, but the financial impact on their wallet is almost always a significant factor in defining "best." A store that tries to sell a card for $10 when the same card can be readily had for $6 online needs to justify the $4 price difference. There may be additional value in immediate accessibility, but there may not.

The other side argues that their LGS prices are not competitive with the market and those stores often try to justify this cost difference due to overhead costs. This argument is typically only known at the micro level; between the person arguing and their LGS owner who is likely not in the debate to begin with, so each instance is very localized.

Unfortunately, this makes it extremely difficult to determine the validity of their concerns. They could be well grounded or they could simply be unhappy with their LGS. In our example above, they view the $10 price tag on a card they can buy online for $6 as the store owner trying to "rip off" their local players. Again the $4 price difference may or may not be justified but the potential buyer views the markup as unreasonable and thus has no interest in making the purchase. The store owner now makes 0% profit instead of whatever they would have had the price been believed to be reasonable from the potential customer.

Why this is Important?

We will now circle back to the Secret Lair series from WoTC. While one could make a fair argument that supplemental products with specific cards included has meant that WoTC has always had a toe in the MTG singles market, the Secret Lair series implies WoTC is willing to dip their whole foot in. One could argue that the Spellbook series was really the initial start of this transition.

However, the big difference here was that the Spellbooks were distributed through LGS's, so they got a share of the profits. The Secret Lair series bypasses the LGS entirely, which is what has rankled so many store owners. To be fair, this is quite justified as they are already being squeezed by non-B&M stores, but nobody can compete with WoTC in the singles market.

Adapt

Everything isn't doom and gloom, though. In the natural world, species that face harsh climates adapt, and so too can the LGS. The LGS environment is definitely a resource store owners can utilize. You have a relatively captive audience, especially during tournaments, which offers a lot of opportunities:

Snacks and Drinks

Many LGS's offer prepackaged snacks and drinks. While they typically won't be making a ton of money off this per transaction, concessions do offer good profit margins when purchased in bulk. Having access to a big bulk store like Costco or Sam's Club allows you to buy these items at a heavily discounted rate, and you can make a 50-75% profit margin while still being competitive with any nearby convenience stores. These profits also tend to scale nicely with tournament attendance.

Inventory Acquisition

As a person who buys and sells cards online, one major challenge I face is acquiring new inventory. All online transactions carry additional risk because they aren't instantaneous: cards can get lost in the mail, people can sell fakes, or even fail to ship out cards. Large stores are willing to shell out thousands of dollars just to set up a few tables at a MagicFest, and for good reason. You can't grow your singles business without consistently acquiring new inventory, and having an actual set, safe location to conduct these transactions can be a vital resource.

I've been to numerous shops where the owner doesn't actively try to pick up cards from patrons and simply waits on them to come up to the store to sell. This likely means that a lot of patrons never trade or sell cards into their LGS simply because they aren't actively trying to get rid of anything. However, when given the opportunity, many players will be happy to move cards they don't really use towards things they do want, though that requires having a good inventory to entice trade-ins.

To be continued...

The LGS business model from the ground up is unnatural and inefficient. In many ways, it’s closer to a glorified clubhouse than a business. And I’m referring to the average LGS, not the dominant players in the eCommerce segment of MTG. The removal of the entry barriers by TCGPlayer was one of the most significant blows to the LGS, and the more recent prioritization of MTG Arena and release of Pioneer to cannibalize Modern was the coup de grâce. I closed my B&M store in 2016 to take a job as a Project Manager and never looked back. I’d been toying with the idea after looking at the industry and seeing the combination of WotC’s business plan and comparing the ability of an LGS to maximize $/sqft vs other industries and it was a no-brainer. I closed while profitable and it was the best decision I ever made. Threat of entrants is one of the most significant dangers to the LGS with players moving more and more to TCGPlayer to buy and sell and playing at home rather than in a store. As competitive magic continues to wither and casual becomes king, the value added by the LGS becomes null. You’re competing against casual players’ comfortable homes with people they can choose and no table fees. This makes it increasingly difficult to monetize floorspace in an LGS when a large portion of it is devoted to “free” space for players. Food and Drink was my third highest revenue generator after online and in store singles sales. In store singles sales accounted for roughly half of online. Food and Drink mainly relies on tournaments, as the casual players are not a captive audience to the extent of grinders. Essentially, as Wizards pushes grinders online, it exponentially accelerates the declines of the traditional LGS. IF I were to ever open a store again (I probably wouldn’t), I’d do three things differently: 1) Offer a monthly membership in exchange for perks specific to being at an LGS–dedicated play space for a playgroup, discount on products etc and unlimited access to demo boardgames. 2) Alcohol–in a state where liquor licenses are often $500,000+, this wasn’t an option. However, in states where it is an option, I’d bring that into the picture. While it violates WotC’s rules for structured competitive play, if you’re not one of the incumbent leaders in competitive play at this point, I’d drop that as a goal from the business model altogether. I only ran Modern, Draft and EDH on the Magic side and EDH was most profitable by far. They tend to be brewing more often and less focused on maximizing value in every tournament they play in. This means you could easily do a gaming bar and still provide space for casual EDH players. 3) If you haven’t caught on already–drastically reduce reliance on MTG altogether. Take the segments that are easy money, but focus on a sustainable business model that is a business first and game store second. I’d even consider putting a big whiteboard on the wall with a monthly “keep the lights on” revenue target if you think your player base would like such a tacky thing. There needs to be an open dialogue between the LGS and its players. Most people don’t understand that WotC has drastically raised the wholesale price on premium and commander products to the point where a new set doesn’t pay 6 months of rent–or even 3 months–and the reality is the sheer existence of an LGS is often an illogical passion project kept alive by personal financing by an owner working another job. I care about money above everything, which made my decision to close the store and put in a more profitable business to that location an easy one. The genie is out of the bottle as far as TCGPlayer’s policy is concerned, and any store that didn’t see it immediately was at high risk of failure. You can’t ask players to come spend 30% more money at your store because you provide value because the reality is, you don’t. The LGS used to have a competitive advangtage in: 1) Singles inventory 2) Sealed product availability and variety 3) Play space. TCGplayer has destroyed 1, eBay and Massdrop have destroyed 2, and Wizard’s push for players to migrate towards Arena coupled with the shift towards casual magic has eroded and will continue to assail 3. If you have a good community (and you are truly lucky if you do) then that is probably the biggest advantage you have over TCGplayer. I remember many retailers making snarky remarks about Amazon like “good luck trying your clothes on over the internet” or even in magic stores “go ask TCGplayer if you can play in their warehouse” and these represent a fundamental misunderstanding of business, the industry and really just people as a whole. The won’t ask TCGplayer–they’ll take the path of least resistance, which will likely be playing together at a kitchen table after all their TCGplayer packages arrive. The reality is, WotC used the LGS to grow and market its game for years and the LGS gobbled it up under the pretense of a symbiotic relationship for years like the turkey getting fattened the months leading up to Thanksgiving and thinking “what a great deal this is”. Magic is growing, but its growth is much less dependent on the LGS now–in fact, if you look at the trends within set and character design alongside WotC’s sentiments regarding the traditional white male gamer, it’s clear that the favorable path is one in which the game’s image can be conveniently censored and replaced with a more “appealing” face of magic in the Arena streaming segment with handpicked personalities.

Wes,

Thank you for this fantastic comment. I appreciate your insights; especially given your history of owning a B&M store. I agree with everything you said on this one. We have one store in our area that is almost entirely Magic and they are struggling to get by. The other one just has Magic on the side and is predominantly a board game store and they are doing fine. I hope any other B&M store owners that read this article also read this comment and consider diversifying their merchandise.

What an incredible comment.